Blog

The CFPB was established on July 21, 2010, under the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act).[i] The CFPB was established as an independent bureau within the Federal Reserve System and is an Executive agency.[ii] Dodd-Frank authorizes the CFPB to exercise its authority to ensure that, with regard to consumer financial products and services:

- Consumers are provided with timely and understandable information to make responsible decisions about financial transactions;

- Consumers are protected from unfair, deceptive, or abusive acts and practices and from discrimination;

- Outdated, unnecessary, or unduly burdensome regulations are regularly identified and addressed in order to reduce unwarranted regulatory burdens;

- Federal consumer financial law is enforced consistently in order to promote fair competition; and

- Markets for consumer financial products and services operate transparently and efficiently to facilitate access and information.[iii]

AUTHORITIES AND FUNCTIONS TRANSFERRED TO THE CFPB

In order to accomplish the declared objectives of the CFPB, certain authorities and functions relating to consumer financial laws were transferred from different agencies to the CFPB.[iv] Certain powers and authorities were transferred from:

- The Board of Governors of the Federal Reserve System

- Office of the Comptroller of the Currency

- Office of Thrift Supervision

- Federal Deposit Insurance Corporation

- National Credit Union Administration

- U.S. Department of Housing and Urban Development

Also, the CFPB has authority – in certain circumstances – under the Federal Trade Commission’s (FTC) Telemarketing Sales Rule and its rules under the FTC Act.[v] And, significantly, the Dodd-Frank Act provided the CFPB with consumer financial regulatory authority.[vi]

As a result, the CFPB altered the consumer financial protection landscape by consolidating rulemaking authority and, to a lesser extent, supervisory and enforcement authority in a single regulator. Consequently, the CFPB has authority over a wide collection of consumer financial products and services.

CFPB’S RULEMAKING POWERS

For purposes of this post, the CFPB’s rulemaking authority is at the core of the discussion outlining the path that led to the “death” of the Arbitration Agreements Rule (the “Rule”). The CFPB is authorized to “prescribe rules and issue orders and guidance, as may be necessary or appropriate to enable the Bureau to administer and carry out the purposes and objectives of the Federal consumer financial laws, and prevent evasions thereof.”[vii]

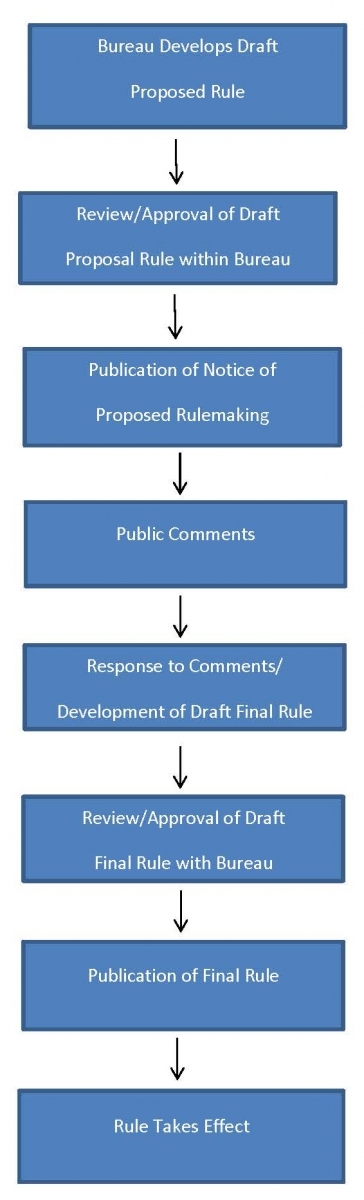

The chart below provides an overview of the CFPB’s typical rulemaking process:

In addition to the steps outlined above, the CFPB is required to convene a small business “advocacy review panel” before proposing regulations that likely will have a “significant economic impact on a substantial number of small entities.”[i] These panels, which are comprised of representatives of the types of small businesses that likely would be affected by regulations, issue reports describing the potential impact of the proposed rule on small businesses.[ii]

THE ARBITRATION AGREEMENTS RULE

The CFPB published the Rule in the Federal Register on July 19, 2017. 12 C.F.R. § 1040, et seq. The Rule would have had two primary impacts on covered providers of certain consumer financial products and services:

- Requiring pre-dispute arbitration agreements to include language expressly permitting a consumer to file a class action in court or to be a member of a class action filed by someone else; and

- Requiring the financial service providers to submit certain arbitration records and court pleadings to the CFPB.[iii]

The Rule established a compliance date of March 19, 2018.[iv] Any pre-dispute arbitration agreement entered into on or after March 19, 2018 would have been required to comply with the Rule. A pre-dispute arbitration agreement was defined in the Rule as an agreement entered into between a consumer and a covered provider requiring the arbitration of any future dispute concerning a covered financial service product or service.[v] The term pre-dispute arbitration agreement included a delegation provision (a provision that provides the arbitrator, not the court, with exclusive authority to resolve any dispute over the enforceability of an arbitration agreement).[vi]

On March 19, 2018, the Rule would have applied to new contracts and to contracts that were transferred between financial service providers.[vii] And, the Rule would have applied to any new financial product or service added to a pre-existing contract (but not to the previously offered product or service).

THE RULE DIES AT THE HANDS OF THE CONGRESSIONAL REVIEW ACT

The Congressional Review Act (CRA), a 1996 law, was intended to make it easier for Congress to overturn administrative action.[viii] The CRA permits Congress to enact a “resolution of disapproval,” which if passed by both houses of Congress and signed by the President, would overturn any rule promulgated by a federal administrative agency.[ix]

On October 24, 2017, the Senate (with a 51 to 50 vote) passed a joint resolution previously passed by the House, disapproving of the Rule. Then, on November 1, 2017, President Trump executed the joint resolution passed by Congress. With the President’s signature, two provisions of the CRA were triggered: First, the Rule “shall not take effect (or continue).” As a consequence, the Rule no longer had the force of law.[x] Second, the CFPB may neither re-issue the Rule “in substantially the same form” nor issue a new rule that is “substantially the same” as the invalidated Rule – unless Congress enacts new legislation “specifically authorizing” such a rule.[xi]

[i][i] 5 U.S.C. §609(d), as amended by the Dodd-Frank Act §1100G.

[ii] Id.

[iii] As defined by the Rule, “class action” meant a lawsuit in which a party seeks or obtains class treatment pursuant to Fed. R. Civ. P. 23 or an analogous State rule.

[iv] 12 C.F.R. § 1040.5 sets forth the compliance date requirement contemplated by the Rule.

[v] See 12 C.F.R. § 1040.2(c). The structure or form of the pre-dispute arbitration agreement does not impact the Rule’s application. Examples include a standalone arbitration agreement, as well as an arbitration agreement that is included within, annexed to, incorporated into, or otherwise made a part of a larger agreement that governs the terms of the product or service. See Official Interpretations to Rule.

[vi] See Official Interpretations to Rule.

[vii] The Official Interpretations to the Rule provided the following illustrative example: Bank A is acquiring Bank B after the compliance date, and Bank B had entered into pre-dispute arbitration agreements before the compliance date. If, as part of the acquisition, Bank A enters into the pre-dispute arbitration agreements of Bank B, Bank A would be required to ensure that the agreements were amended to contain the mandatory provision, the alternative provision, or to provide the notice specified in section 1040.4(a)(2)(iii)(B).

[viii] 5 U.S.C. §§ 801-808.

[ix] 5 U.S.C. § 801.

[x] 5 U.S.C. § 801(b)(1).

[xi] 5 U.S.C. § 801(b)(2).

[i] See CFPB Strategic Plan, Budget and Performance Plan and Report (May 2017), p. 4.

[ii] Id.

[iii] Id.

[iv] Id.

[v] Id.

[vi] Id.

[vii] Dodd-Frank Act §1022(b), 12 U.S.C. §5512(b).

Attorneys

AttorneysStephen is a Shareholder and member of the Complex and Commercial Litigation practice group. His expertise lies in handling of complex issues and disputes at all levels and stages, including analyzing potential risks, resolving ...