“This Ain’t the Summer of Love”: The SEC’s new “Pay versus Performance” Disclosure Rules

The Securities and Exchange Commission continued its busy summer of rulemaking on August 25th when it issued final “Pay versus Performance” disclosure rules, which were originally proposed back in 2015 and are required under the Dodd-Frank Act. And, if you are like most companies and advisors who now have just a few months to calculate executive compensation “actually paid” to their named executive officers (NEOs), identify the most important financial measures used to link pay and performance, and describe a number of relationships between compensation actually paid and various metrics (including the company’s cumulative total shareholder return (TSR) over five years), among other requirements, there is not a lot to love. The “Pay versus Performance” rules will likely become final in late September 2022 and, to the surprise of some, these substantial new disclosures will be required in companies’ 2023 proxy statements. Compliance with the new rules – housed in a new Item 402(v) of Regulation S-K – will require a significant amount of work from management and their advisors, and while that heavy lift is reason enough for everyone to start preparing now, there’s an even more pressing reason: these disclosures might motivate your compensation committee to make adjustments to your compensation program for 2023, so the time to draft these new disclosures isn’t during proxy season, it’s now. As Blue Oyster Cult says, “things ain’t like what they used to be, and this ain’t the summer of love.”

What are the most significant new disclosures?

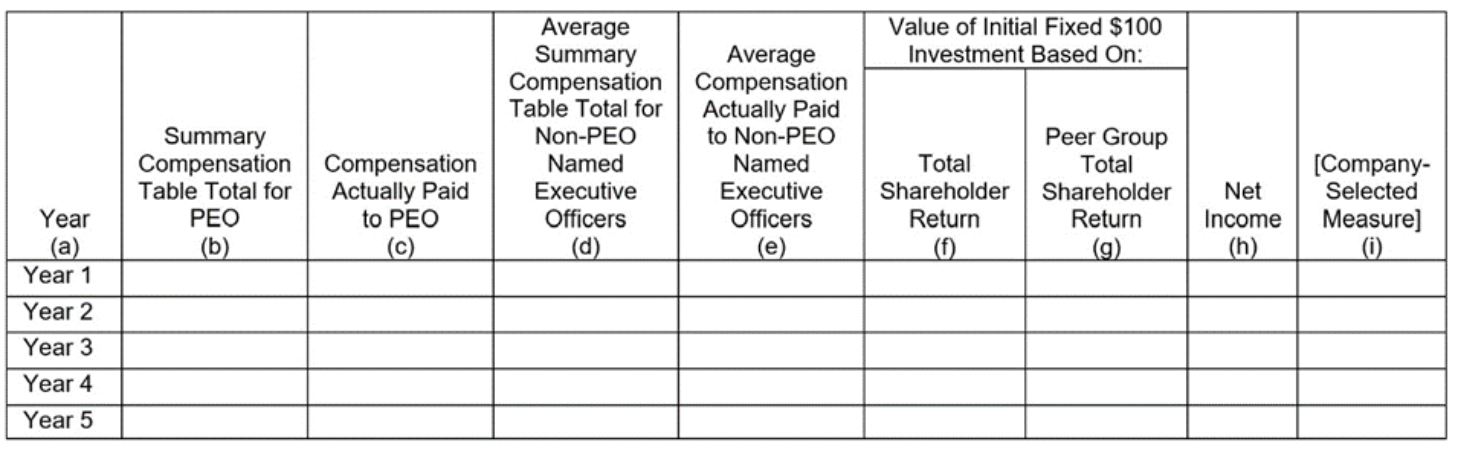

1. The “Pay Versus Performance” table. In 2023, companies will be required to provide the following table for the last three most recently completed fiscal years, with an additional year of disclosure added in each of 2024 and 2025:

The rules specify how to calculate “compensation actually paid” (columns (c) and (e) above), but the calculation will involve making a number of adjustments to the total compensation number disclosed in the Summary Compensation Table (SCT) for equity awards and pension benefits. These changes include (i) deducting the equity award amounts reported in the SCT and adding the year-end fair value of any equity awards that were granted in the subject year, adding the change in fair value of any awards granted in prior years that are outstanding or that vest during the subject year, and subtracting the fair value of equity awards granted in prior years that fail to meet the vesting conditions during the subject year; and (ii) deducting the change in actuarial present value of all defined benefit and pension plans and adding actuarially determined service cost and prior service cost. Companies must provide footnoted disclosure of the amounts that were deducted from, and added to, the SCT amounts to calculate the compensation actually paid and vesting date valuation assumptions.

The new “Company-Selected Measure” (CSM) appearing in the table (column (i) above) is required to be the financial performance measure that, in the company’s assessment, represents the most important performance measure used by the company to link compensation actually paid to the NEOs in the last fiscal year to company performance. The SEC defines “financial performance measure” as any measure determined and presented in accordance with the company’s accounting principles, any measures that are derived from such measures, stock price and TSR, other than measures otherwise required to be disclosed in the “Pay Versus Performance” table.

It is worth noting that companies may cover additional years in the table so long as the disclosure is not misleading. Companies may also supplement the table with additional performance measures so long as the measures are clearly identified as supplemental, not misleading, and not presented with greater prominence than the required disclosure.

2. The “clear descriptions of relationships” disclosure. Using the information in the “Pay Versus Performance” table, companies must provide clear descriptions, in graphical and/or narrative format, of a number of relationships, in each case over the five most recently completed fiscal years (subject to the phase-in period described above). The relationships that must be discussed include those between (i) the amount of compensation actually paid to the principal executive officer (PEO) and (ii) the average actual compensation paid to the other NEOs, on the one hand, and the company’s cumulative TSR, the company’s net income, and the company’s CSM, on the other hand. These descriptions must also include a comparison of the company’s cumulative TSR to that of its peer group over the same period. Any additional measures that are included in the “Pay Versus Performance” table must be accompanied by a description of the relationship between the compensation actually paid to each of the PEO and the other NEOs to such additional measures.

3. The tabular list of “most important financial performance measures” used to link pay and performance. Companies must also provide a tabular list of the three to seven most important financial performance measures, including the CSM, used to link compensation actually paid to company performance. This information can be presented in one tabular list, two separate lists (one for the PEO and one for all of the other NEOs) or separate lists for the PEO and each other NEO. If the company used fewer than three financial performance measures to link compensation to performance for the most recently completed fiscal year, the list must include all such measures that were used. A company may include non-financial measures if it determines that such measures are among its three to seven most important performance measures and it has disclosed its most important three (or fewer, if applicable) financial performance measures. For these purposes, financial measures that are considered non-GAAP financial measures will not be subject to Regulation G or Item 10(e) of Regulation S-K, but the company must disclose how the number is calculated from its audited financial statements.

4. Inline XBRL Tagging. Companies will be required to separately tag each value disclosed in the “Pay Versus Performance” table, block-text tag the footnote and relationship disclosure, and tag specific data points (such as quantitative amounts) within the footnote disclosures, all in Inline XBRL, beginning with their 2023 proxy statements. Smaller reporting companies are not required to comply with the Inline XBRL requirement until their third filing containing pay versus performance disclosure.

The “Pay versus Performance” rules will become effective thirty days after publication in the Federal Register and companies must comply with the rules in proxy and information statements that are required to include Item 402 executive compensation disclosure for fiscal years ending on or after December 16, 2022. Smaller reporting companies have scaled disclosure requirements, and emerging growth companies and foreign private issuers are exempt from the “Pay Versus Performance” table and the other disclosures called for under the new rules.

What should public companies do now (like, right now)?

Maynard’s Public Company Advisory team recommends that management, compensation consultants, compensation committees and other advisors put together (now) drafts of the “Pay Versus Performance” table, the “clear descriptions of relationships” disclosures and the tabular list of the most important financial performance measures used to link compensation actually paid to company performance utilizing historical data. Even though 2022 data will need to be added to the disclosure, having a picture of what the table and relationship graphs might look like will enable the various parties to get a head start on drafting the accompanying narrative. For most companies, providing a clear description between compensation actually paid and the prescribed performance measures will be challenging, as many compensation committees do not evaluate compensation on this basis and they might want to consider adding supplemental measures that reflect how they actually view the connection between compensation and performance. Finally, as noted above, the “Pay Versus Performance” table and related disclosures might motivate changes to certain aspects of the compensation program for 2023, so this information should be provided to compensation committees soon in order to enable those conversations. It’s time to leave this summer behind and get to work.

For additional information about any of the above developments, or to discuss any questions that you may have, please contact a member of Maynard’s Public Company Advisory Group.

About Maynard Nexsen

Maynard Nexsen is a full-service law firm with more than 550 attorneys in 24 offices from coast to coast across the United States. Maynard Nexsen formed in 2023 when two successful, client-centered firms combined to form a powerful national team. Maynard Nexsen’s list of clients spans a wide range of industry sectors and includes both public and private companies.